Enjoy 10% off charging at all public Charge+ locations for 3 months.

Living in a condo with Charge+ chargers? Get 1 month of Nano-tier access for free.

Includes comprehensive protection, windscreen claims, and reliable claims support.

If you insure your Tesla with ECICS, you also receive complimentary Tesla fractional shares—stackable with Charge+ benefits. Want to find out more? Click here

.png)

(same mobile number linked)

Terms and conditions apply. Discount is automatically applied. Not stackable with other promos.

We’re More Than Just an Insurer—We’re Your Neighbour Through Life’s What-Ifs.

The Insured Person must be: - a resident of Singapore who is permanently residing in Singapore; and - between 18 and 65 years old (both inclusive) at the time of application.

In the event of any loss or damage, your insurer for your primary insurance policy must have paid out a claim amount higher than your policy excess in order to seek reimbursement on the excess from your ECICS Non-Motor Excess Protector Insurance Policy. If the claim amount paid out is lower than your policy excess, you will not be able to seek reimbursement from your ECICS Non-Motor Excess Protector Insurance Policy.

Please declare all claims (excluding windscreen claims) made against your private car insurance during the past 3 years.

A No-Claim Discount (‘NCD’) is an entitlement given to you if no claim has been made under your policy for a year or more with the current/existing insurer. It reduces the premium you have to pay for the following year. This is your insurer's way of recognising and rewarding you for having been a careful driver. There is a standard followed by all insurers in setting the NCD, depending on your type of vehicle (private, commercial or motorcycle) and the period of insurance with no claim. The following table shows how the NCD is set by all insurers across the industry. Private Car Period of insurance with no claim Discount on renewal 1 year 10% 2 years 20% 3 years 30% 4 years 40% 5 years or longer 50% Motorcycle/Commercial Vehicle Period of insurance with no claim Discount on renewal 1 year 10% 2 years 15% 3 years or longer 20%

No, while its not compulsory, it’s strongly recommended to protect your business from legal and financial liability if someone is injured or property is damaged due to your operations.

No, she is not covered unless she is travelling with you. We recommend purchasing a separate travel insurance for your FDW as the coverage would be more comprehensive for overseas situations where medical and evacuation costs are expected to be much higher.

Yes, you can. We offer Waiver of Counter Indemnity as an optional add-on. With this, your liability on the $5,000 Security Bond is capped at $250, and the insurer covers the rest if the bond conditions are breached. However, this does not apply to any breach of bond conditions due to your negligence or fault.

• Outpatient Medical Expenses (For Accident) cover medical bills for outpatient treatments that arise solely from Accident. For example, your FDW accidentally scalds her hand while cooking and requires dressing for the burn.• Hospital & Surgical Expenses cover inpatient medical bills for treatments related to both accidents and illnesses.

To implement for MI policies, renewals or extensions with start date effective from:1 July 2023 (Stage 1)• Introduction of a co-payment element* for employers and insurers for amounts above $15,000, up to an annual claim limit of at least $60,0001 July 2025 (Stage 2)• Standardisation of allowable exclusion clauses• Introduction of age-differentiated premiums for those aged 50 and below, and those aged above 50• Requirement for insurers to reimburse hospitals directly upon the admissibility of the claimPlease visit MOM's website here for more information on the MI enhancements.

No. The Security Bond is included in our Enhanced MaidAssure along with MOM’s minimum medical and personal accident insurance as a package. We do not offer just the Security Bond.

We do not cover usage for food, parcel or other delivery services.

Excess, also known as the deductible, is the first amount of the claim that the policyholder needs to bear in view of the claim.

A No-Claim Discount (‘NCD’) is an entitlement given to you if no claim has been made under your policy for a year or more with the current/existing insurer. It reduces the premium you have to pay for the following year. This is your insurer's way of recognising and rewarding you for having been a careful driver. There is a standard followed by all insurers in setting the NCD, depending on your type of vehicle (private, commercial or motorcycle) and the period of insurance with no claim. The following table shows how the NCD is set by all insurers across the industry. Private Car Period of insurance with no claim Discount on renewal 1 year 10% 2 years 20% 3 years 30% 4 years 40% 5 years or longer 50% Motorcycle/Commercial Vehicle Period of insurance with no claim Discount on renewal 1 year 10% 2 years 15% 3 years or longer 20%

Yes, you can include as many named drivers as you want in your Private Motor Car insurance policy subject to underwriting and additional premium.

The driver involved in the accident must report personally, with a copy of the Driving License and NRIC, and the certificate of insurance to the Accident Reporting Centres. The vehicle must also be made available for photo-taking at the time of reporting.

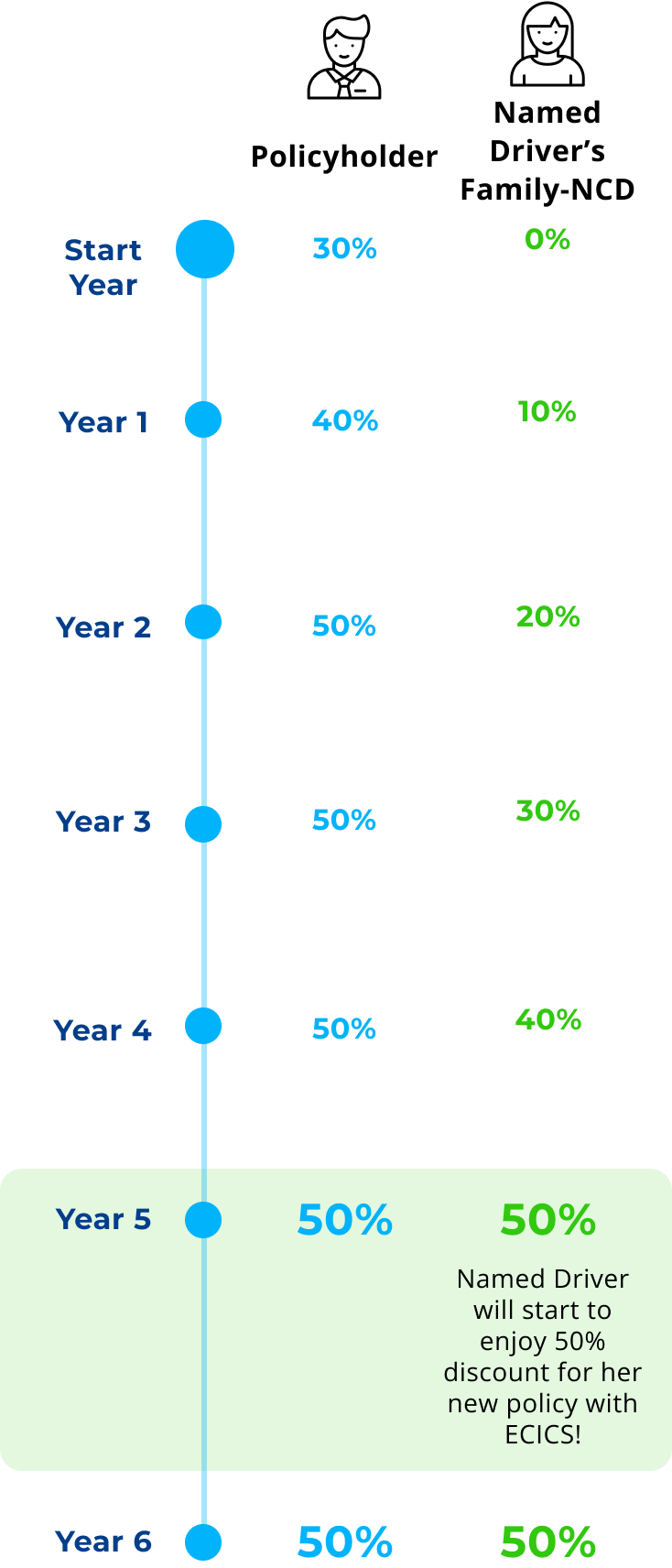

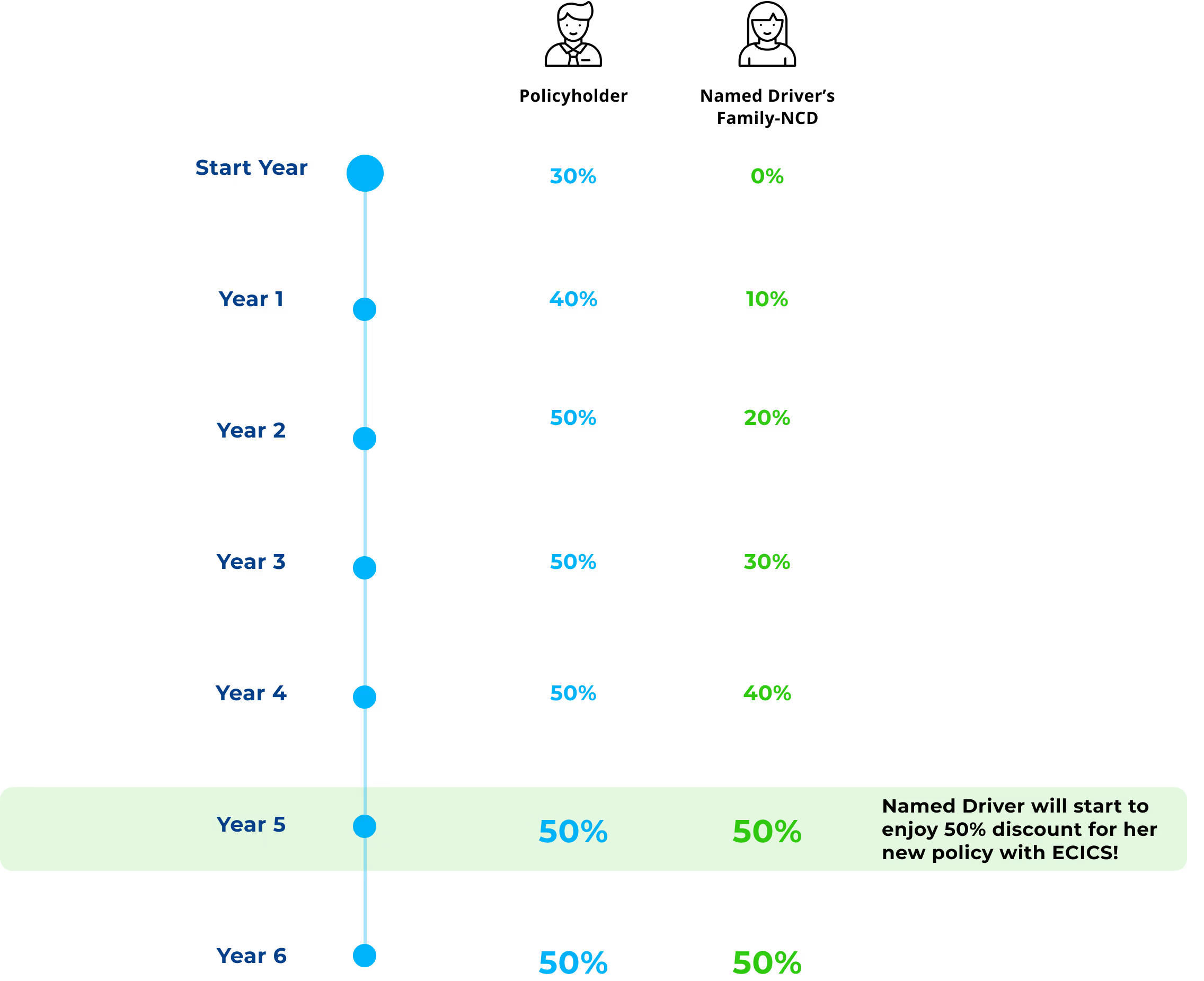

All earned Family-NCD will be reduced according to the GIA NCD framework (https://gia.org.sg/). However, with the Family NCD benefit still in place, it means all the Family NCD members can continue to earn 10% with each year of safe driving (max at 50%).

.png)